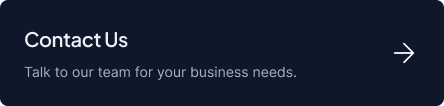

Try The Leave Encashment Calculator

Add the average of your Basic Salary + DA for the last 10 months

Tax-Free Amount

₹ 0

Total Leave Encashment

₹ 13,333

Taxable Salary Amount

₹ 13,333

What is a leave encashment calculator?

A leave encashment calculator helps estimate the amount payable to an employee for unused paid leave. This is generally used when workers wish to determine how much their leave is worth, while on the other hand, HR or payroll departments use it for calculation during salary settlements and more.

For employees

It gives employees a quick estimate of the amount they may receive for unused leave during settlement or payroll processing.

For businesses

It supports payroll planning and helps reduce confusion around leave balances, encashment eligibility, and settlement amounts.

The calculator usually takes into account factors like:

In many cases, earned leave or privilege leave is considered for encashment, depending on the company's leave policy.

This should be used as an operational calculator for estimation. Final leave encashment should always be checked against company policy, employee category, leave balance records, employment terms, and applicable tax rules.

How to use the leave encashment calculator

To use the leave encashment calculator, enter the required salary and leave balance details. The calculator will estimate the payable amount based on the values added.

Start by adding the salary amount used for leave encashment calculation. In many cases, this may be based on basic salary and dearness allowance, but the exact salary component depends on company policy and applicable rules.

HR and payroll teams should avoid using gross salary unless the policy specifically allows it.

Enter the unused eligible leave balance and total leaves allowed per year based on company leave policy. Only leave that is eligible for encashment should be included in the calculation.

Choose employee type, when leave is encashed, and years of service. These inputs help estimate exemption and taxable leave salary based on commonly used tax treatment rules.

Once the inputs are added, the calculator shows estimated exemption, leave encashment available, and taxable leave salary. Use this for planning, but verify the final amount against policy and payroll records before processing.

Leave encashment formula

The commonly used formula for leave encashment calculation is:

The Formula

This formula calculates the value of unused eligible leave based on the employee's monthly salary components and leave balance.

- Basic Salary + Dearness Allowance refers to the salary components considered for leave encashment. In many cases, leave encashment is calculated on basic salary and DA, but organisations should confirm the salary basis from their leave policy or payroll rules.

- Number of Unused Eligible Leaves refers to the leave balance that can be encashed. Usually, earned leave or privilege leave is considered, but eligibility depends on the organisation's policy.

- 30-day salary basis is commonly used to calculate the per-day value of salary for leave encashment.

For Example:

So, the estimated leave encashment amount will be ₹30,000.

The formula is simple, but the final calculation should be supported by accurate leave records, correct salary components, policy limits, and tax validation before payroll processing.

Leave encashment calculation example

Here is a simple example of how leave encashment calculation works for an employee with unused earned leave.

Example: Leave encashment for an employee with unused earned leave

- First, calculate the per-day salary value:

Per-Day Salary = Basic Salary + DA ÷ 30

₹45,000 ÷ 30 = ₹1,500 per day

- Now apply the leave encashment formula:

Leave Encashment = Per-Day Salary × Unused Eligible Leaves

₹1,500 × 20 = ₹30,000

So, the estimated leave encashment amount will be ₹30,000.

This example is useful when you want to calculate leave encashment online for a quick estimate. In actual payroll, the final amount may change based on company leave policy, salary components, employee category & carry-forward limits

Which types of leave can be encashed?

Not every leave balance is automatically eligible for encashment. In most organisations, leave encashment is usually linked to earned leave or privilege leave because these leaves are accumulated over a period of service.

Common leave categories include:

- Privilege Leave/Earned Leave: Generally encashable, depending on the policies of the organization.

- Casual Leave: Generally utilized for short-term personal reasons; may expire if not used.

- Sick Leave: Usually meant for medical absence and may not always be encashable.

- Compensatory Off: Adjusted based on the additional number of days worked; has different guidelines applicable to it.

- Special Leave: Eligibility depends on the internal policies of the organization.

Leave encashment validation

Other leave types may follow different rules. Casual leave, sick leave, maternity leave, compensatory off, or special leave may or may not be encashable depending on the organisation's policy.

This implies that the leave carry forward balance as reflected in the system is not always going to be the same as the encashable leave balance. The critical point for HR and payroll departments is to identify which leave balances can be carried forward, which leaves lapse, and those that can be encashed during service or termination.

Leave encashment tax rules in India.

Leave encashment tax treatment in India depends on the employee type and when the leave is encashed. Tax treatment may differ for government employees and non-government employees, and it may also differ when leave is encashed during service versus at retirement or resignation.

For government employees; Income Tax Act — Section 10(10AA)

Leave encashment received by government employees at retirement is generally treated as fully exempt under Section 10(10AA), subject to applicable tax rules.

For non-government employees

The exempt amount is generally the least of the applicable exemption limit, actual leave encashment received, salary-based calculation, or cash equivalent of unavailed leave.

For payroll teams

Payroll teams should review employee type, encashment timing, salary details, exemption limits, leave balance, and tax treatment before processing the final payout or settlement amount.

Before final processing, teams should check.

This section should be treated as general information, not tax advice. Employees and employers should verify the latest tax rules, payroll policy, and professional tax guidance before final salary or full and final settlement processing.

Leave encashment during service vs at retirement

Leave encashment can be handled differently depending on when it is paid. The two common situations are leave encashment during service and leave encashment at the time of resignation, retirement, or full and final settlement.

This timing is important because the same balance of leave will have different accounting or tax treatments if paid either within the employment period or upon termination. Businesses need to ensure that their record keeping for leave is up to date prior to salary closure.

During service

When leave is encashed during service, it is usually treated as part of regular salary processing. The amount may be paid based on company policy, leave balance, grade-level rules, and payroll cycle.

In many organisations, encashment during service is allowed only after a minimum leave balance is maintained.

At retirement

At the time of resignation/retirement, the encashment of leaves is normally done during the final settlement process. In such a scenario, the HR & Payroll department has to be sure about the following aspects of an individual.

Common mistakes that affect leave encashment calculation accuracy

Leave encashment errors usually happen when salary basis, leave balance, policy rules or tax treatment are not checked properly. A structured review helps avoid incorrect payouts during payroll or full and final settlement.

Using the wrong salary basis

Leave encashment should be calculated on the applicable salary components, not always on gross salary.

Including non-encashable leave types

Not every leave balance can be paid out. Earned leave or privilege leave is usually considered, but other leave types may follow different rules.

Ignoring carry-forward limits

Leave balances should be checked against carry-forward and encashment limits before calculation.

Not updating leave balance before settlement

Pending leave approvals, manual corrections, or unprocessed attendance records can change the final balance.

Missing tax treatment checks

The taxable and exempt portion should be checked with thorough attention before final payroll or full and final settlement.

Applying same rule for every employee

The same calculation rule may not apply to every employee, as eligibility can depend on policy, tenure, location and payout timing.

Using the wrong salary basis

Leave encashment should be calculated on the applicable salary components, not always on gross salary.

Ignoring carry-forward limits

Leave balances should be checked against carry-forward and encashment limits before calculation.

Missing tax treatment checks

The taxable and exempt portion should be checked with thorough attention before final payroll or full and final settlement.

Including non-encashable leave types

Not every leave balance can be paid out. Earned leave or privilege leave is usually considered, but other leave types may follow different rules.

Not updating leave balance before settlement

Pending leave approvals, manual corrections, or unprocessed attendance records can change the final balance.

Applying same rule for every employee

The same calculation rule may not apply to every employee, as eligibility can depend on policy, tenure, location and payout timing.

A reliable leave encashment calculation should always start with verified leave balance, correct salary components, clear policy mapping, and proper payroll validation.

Why accurate leave encashment calculation matters for clear payouts

Incorrect leave encashment impacts the payment to the employees, the payroll process, and settlement. Wrong calculation of the leave encashment may result in disputes, payroll errors, tax issues, and delay in the processing of settlements.

For employees

Accurate leave encashment helps employees understand the value of unused paid leave, how the amount is calculated, and which leave balance was considered.

For businesses

Accurate leave encashment helps businesses calculate payouts correctly, verify leave eligibility, and reduce payroll confusion during settlement or salary processing.

Accurate leave encashment calculation helps businesses improve:

For large organisations, leave encashment should not be handled as a one-time manual calculation. It should be connected with leave policy, approval records, attendance data, payroll rules, and settlement workflows.

Managing leave encashment at enterprise scale

For small teams, leave encashment may be checked manually during payroll or exit processing. For big organizations, this becomes a little difficult due to the differences in the leave policy depending on the location, level, employee classification, business division and method of settlement of employment terms.

Both HR and payroll must verify that the employee has a balance that is available for leaves, if the type of leave is encashable, salary heads that are applicable, and whether the process of payment is happening during employment or at the time of full and final settlement.

A structured leave management and payroll process helps maintain accurate leave records, apply policy rules consistently, and pass verified inputs to payroll. For enterprises managing multiple locations and employee categories, Ascent helps bring better control over leave balances, encashment eligibility, and payroll-linked workforce operations.

At enterprise scale, leave encashment depends on:

When these inputs are handled separately, errors become common. A wrong leave balance, outdated policy rule, or incorrect salary basis can affect the final payout and create employee disputes.

FAQs

Find answers to practical questions about leave encashment calculation, salary basis, eligible leave types, and tax treatment.

Leave encashment is usually calculated by finding the per-day salary value and multiplying it by the number of unused eligible leaves.

Formula:

Leave Encashment = (Basic Salary + DA) ÷ 30 × Unused Eligible Leaves

The actual calculation may vary based on company policy, employee category, and applicable rules.

In many cases, leave encashment is calculated using Basic Salary + Dearness Allowance. However, the exact salary basis depends on the company's leave policy, employment terms, and applicable rules.

HR and payroll teams should avoid using gross salary unless the policy clearly defines it as the calculation basis.

The most common types of leaves for encashing are earned leave or privilege leave. Other types of leaves such as casual leaves, sick leaves, compensatory off, or special leaves may not necessarily be encashable. It all depends on the policies set by the organization.

Taxation of leave encashment by an individual in India may vary based on the category of the individual and the time of leave encashment. There may be variations in tax law concerning leave encashment by both governmental and non-governmental employees.

It is necessary to check the tax requirements before making the payments.

This calculator should be used as an operational calculator for estimation. Final payroll or full and final settlement should be processed only after checking verified leave balance, encashment eligibility, salary components, company policy, employment terms, and applicable tax treatment.